The Ukrainian government bond market showed a rapid increase in volume in 2019, helping the government significantly improve its debt indicators which has been weighing quite heavily on the country.

We speak to Konstantin Stetsenko, Founding Partner at ICU, the leading asset manager in Ukraine, to find out what caused the rally and whether he expects it to continue into 2020.

Konstantin Stetsenko, ICU

Konstantin Stetsenko, ICU

Who’s behind the rally?

Konstantin: The increase in local bond volumes was driven mainly by international investors last year. International investors became active buyers of local government bonds in anticipation of a stronger hryvnia and a decrease in National Bank of Ukraine discount rate. This has helped drive the increase in international investors holdings domestic bonds up to $5bn, compared with just $0.2bn in 2018. International investors have also shifted from investing in shorter term maturities, preferring bonds with 2 to 3-year tenors.

What caused the surge in volume last year?

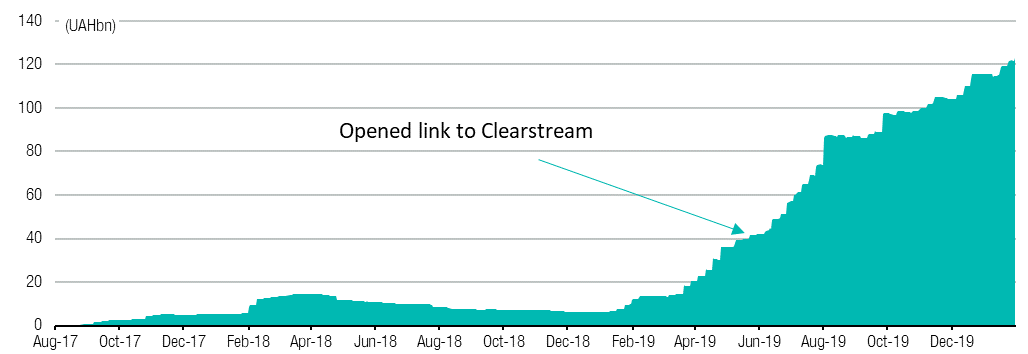

Konstantin: The 2019 boom was partly enabled by the introduction of the Clearstream link, which was set up by the Ministry of Finance and the National Bank of Ukraine (NBU) at the end of May. This helped simplify the trading process massively. Previously, foreign investors had to go through a lot of bureaucratic layers to trade local bonds. They had to open an account with a Ukrainian bank and conclude an agreement with a local broker, followed by other lengthy procedures. Since the introduction of Clearstream link, however, they now have direct access to papers through a generally accepted international system. Last year alone, international investors have bought $4.8bn in local paper, accounting for 14.2% of outstanding domestic bonds.

Source: NBU, ICU

Was this part of the reform process?

Konstantin: Yes, international investors have been in the hunt for yield in a low interest rate environment, but they would not have sought to invest in Ukraine if they didn’t believe the reforms are taking effect. Furthermore, they would have invested without the support of the IMF. IMF support is an important validation that the reforms are working in gradually opening the market and highlight that Ukraine is open for investment.

Was the Clearstream link the main reason behind the rally?

Konstantin: The Clearstream link has been an important step in opening up the local market to international investors. Another key development last year was that investors could finally participate in government bond auction market through the Bloomberg terminal.

What is the significance of being able to trade through the Bloomberg terminal?

Konstantin: This was an important development as trading through the platform not only increases market transparency and accountability but also provides access to the primary market through an international depository.

And how has this affected the hryvnia?

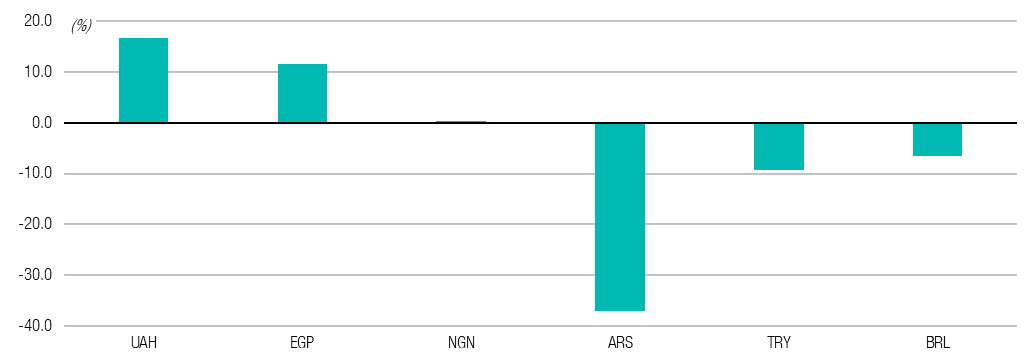

Konstantin: A large influx of funds from outside of Ukraine, which was accompanied by the sale of currency in Ukraine, has enabled the hryvnia to significantly increase its position and become one of the best-performing currencies in the world last year.

At the end of 2019, the hryvnia exchange rate growth amounted to 16.6%. For comparison, the Egyptian pound was 11.7%, for the Nigerian naira – 0.4%, while the Argentine peso, the Brazilian real and the Turkish lira lost 37%, 6.5% and 9%, respectively.

Source: Bloomberg, ICU

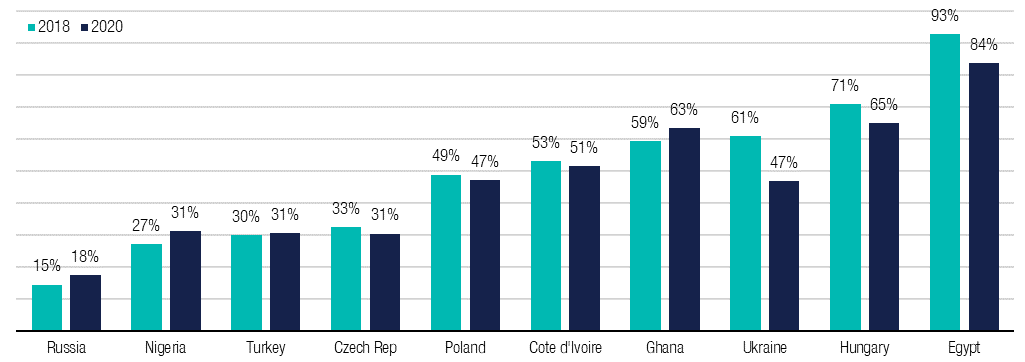

Where does Ukraine rank in comparison to its peers in terms of international investors in the domestic markets?

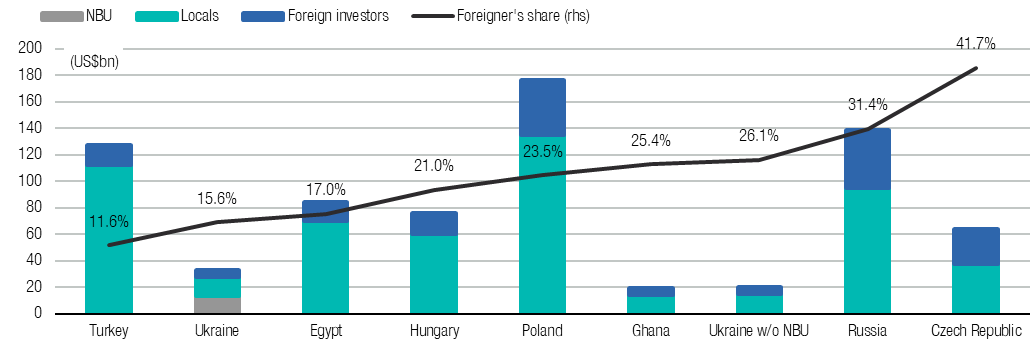

Konstantin: If we compare Ukraine with other similar countries with developing economies, international investors’ share of public debt in Ukraine is only slightly higher than Turkey (see chart below). But it is still significantly lower than other countries, the closest of which will be Hungary, Egypt and Poland.

If we exclude the NBU portfolio, which is more than 40%, from the total volume of issued government bonds, then Ukraine will move above these countries by the share of foreign investors.

Similarly, the participation of foreigners in the hryvnia debt will still be lower than that of Russia or the Czech Republic. In nominal terms, total debt and foreigners’ participation are the smallest across these countries.

Source: NBU, countries’ national banks, ICU

What does the international participation mean for the local bond market?

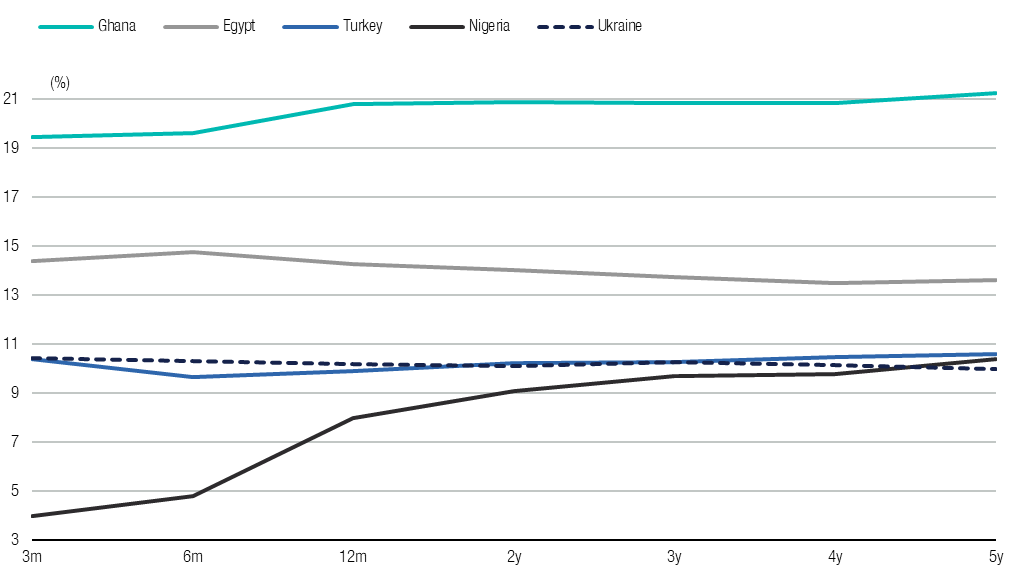

Konstantin: Foreigners’ participation in local market has allowed Ukrainian Ministry of Finance to decrease interest rates for local-currency debt from 19-21% at the beginning of last year, to 10-11% at the beginning of 2020. Now yield curve for UAH-denominated debt is very close to the level of rates for local-currency debt in Nigeria and Turkey, and below Egypt and Ghana.

On the one hand, low rates for local-currency debt indicates lower risks of investments, while on the other hand, it helps the government decrease its cost of debt service, using less revenue for it.

Source: Bloomberg, ICU

And how does that help Ukraine’s overall economy?

Konstantin: Local currency appreciation with increase of its share in total debt allowed also improved country’s debt indicators. While at the end of 2018 Ukraine’s debt-to-GDP ratio was at 61%, at the end of last year it declined to about 51%, according to reported by the Ministry of Finance debt statement and amount of GDP forecasted by ICU research. This year this indicator can drop to around 47%. Compared with other countries from eastern Europe, according to IMF forecasts, at the end of 2020 Ukraine’s debt-to-GDP ratio will be close to Poland, but higher than the Czech Republic and Turkey. But it will be lower than in Hungary, Ghana and Cote-d’Ivoire. Compared with Egypt, Ukraine just blooming as in Egypt debt-to-GDP ratio this year will be at around 84%, according to IMF forecast. This ultimately means that Ukraine is not only reliant on IMF loans to pay off its debt.

Source: WEO, MoF, State Statistics Service of Ukraine, ICU

Do you expect this trend to continue in 2020?

Konstantin: The current macro environment coupled with positive debt dynamic with lower inflation and easing monetary policy will continue to draw the attention of international investors to UAH-denominated debt. We expect a further increase in foreign investments during this year. According to our assumptions, foreigners will likely invest an additional UAH50bn (around US$2bn) this year and increase their portfolio to about UAH170bn (US$7bn).

What other reforms can we anticipate?

Konstantin: The Ministry of Finance and NBU are going to continue with the reform implementation as the development of the capital markets is a core part of the mid-term strategy in the financial sector reform development.

The plan for the next few years is to issue only local-currency denominated bonds in domestic bonds market. They also are looking to be included in the JPMorgan GBI-EM index. The Ministry of Finance and NBU also intended to provide access for foreign investors to primary bonds market through international custody, thereby widening a list of custody, with link to Euroclear, significantly increasing the investors base.

So far, we have only discussed primary markets—what about a secondary market?

Konstantin: The plan is to also develop a secondary bonds market to make the bond market more liquid and increase the number of trades. In 2019, the number of deals at stocks exchanges rose by 20% to UAH295bn (about UA$12bn) or 97% of total turnover at stocks exchanges. OTC market has also been very active.

To develop the OTC market, Bloomberg together with other key primary dealers are working closely to establish a new platform for trading with Ukrainian T-bills in the secondary market. Taking into the account, the new platform should simplify trading with investors and provide additional transparency, increase the liquidity of Ukrainian T-bills.

Konstantin Stetsenko concludes the interview by saying that the year looks promising for the development of the bond markets and that we must not take our eye off the ball and Ukraine should keep forging on with the reform process to further boost investor confidence.